UAE Free Zone vs Mainland 2026: Where to Invest?

For foreign investors entering the UAE in 2026, the choice between a free zone and the mainland is no longer a simple trade-off between tax savings and market access. New rules now let free-zone companies operate onshore, while corporate tax and the global minimum tax have raised the stakes on getting the structure right from day one.

The United Arab Emirates remains one of the easiest and most attractive places in the world to start a business, but in 2026 the structural decision behind that setup carries more weight than ever. Federal corporate tax is now an established part of the landscape, a 15 percent global minimum tax applies to large multinational groups, free-zone qualifying-income rules have matured into an annually tested compliance position, and a landmark 2025 reform has begun to dissolve the old wall between free-zone and mainland business.

For foreign investors, the result is a richer but more demanding set of choices. This article compares the two principal routes (mainland and free zone) across ownership, market access, tax treatment, costs, and compliance, and sets out a practical framework for deciding where to invest in 2026.

The 2026 context: A market still pulling in record capital

The backdrop to this decision is a UAE economy that continues to attract foreign capital at record pace. Dubai drew an estimated AED 52.3 billion (US$14.24 billion) of foreign direct investment (FDI) in 2024, up 33.2 percent year on year, alongside a record 1,117 greenfield projects, keeping it first in the world for greenfield FDI for a fourth consecutive year.

Momentum carried into 2025. In the first half of the year, Dubai attracted roughly US$11 billion in FDI capital, up around 62 percent on the same period a year earlier — and a record 643 greenfield projects, the highest half-year tally since tracking began in 2003. The emirate climbed to second globally for total FDI capital and held the top spot worldwide for headquarters projects, with particular strength in artificial intelligence and fintech.

What changed in 2026: The free zone–mainland wall starts to fall

The single most important structural development for this decision is Dubai Executive Council Resolution No. 11 of 2025. Historically, a free-zone company could not sell directly into the UAE domestic market; reaching mainland customers meant appointing a local distributor or agent, or setting up a separate mainland entity, often duplicating filings and cost.

Under the new framework, most non-financial free-zone companies in Dubai can now operate on the mainland by obtaining either a branch licence (valid for one year and renewable) or a temporary permit (for specific activities of up to six months) from the Department of Economy and Tourism (DET). Permit and branch fees typically run between AED 5,000 and AED 10,000, and the activity must fall within the approved list DET published in September 2025.

Financial institutions in the Dubai International Financial Centre (DIFC) are excluded and remain under separate oversight.

The practical effect is significant: a single legal entity can increasingly serve both international and domestic markets without restructuring. Companies already trading on the mainland before the resolution were given until early March 2026 to regularise their status.

For new investors, the reform softens what used to be the free zone’s biggest drawback (limited domestic reach) and shifts the decision toward tax position, activity type, and long-term structure rather than market access alone.

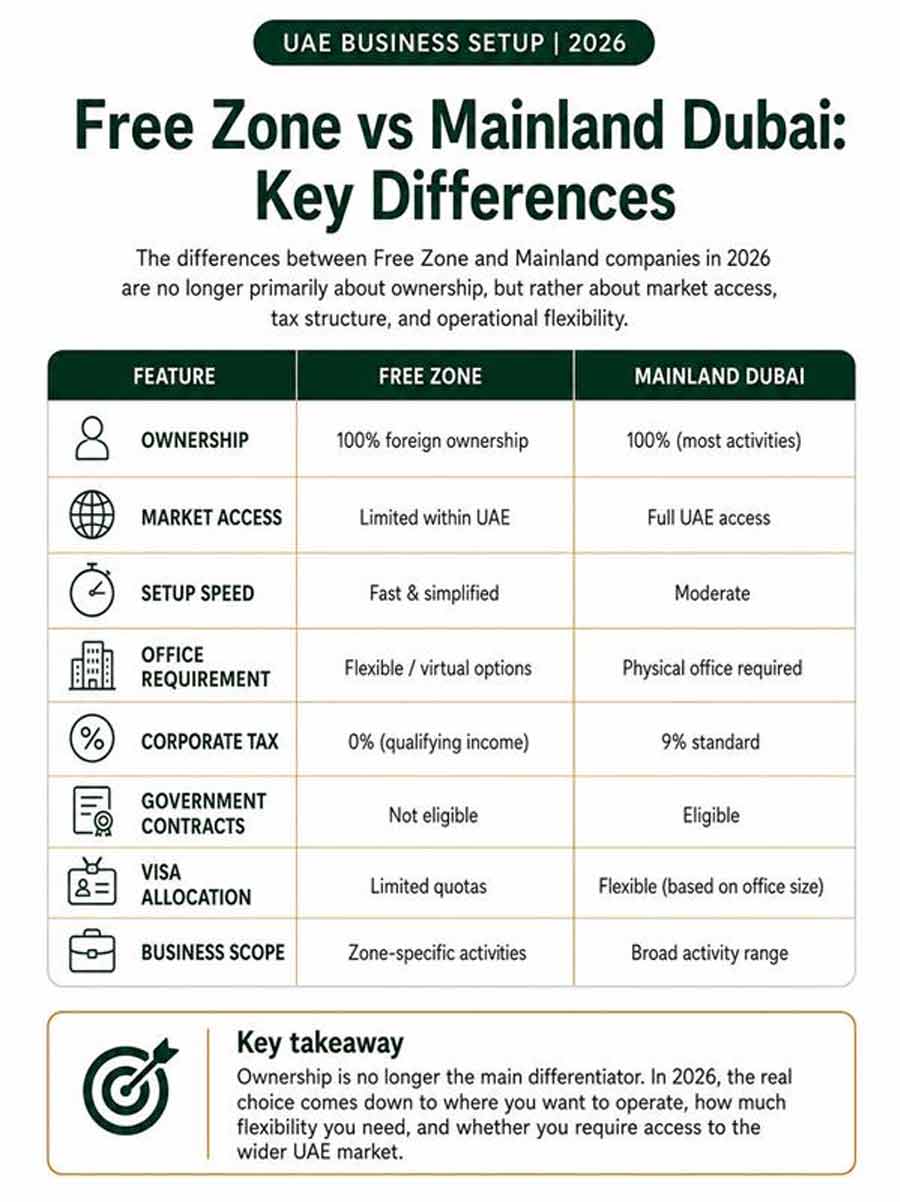

Foreign ownership: No longer a differentiator

For most of the past decade, the defining advantage of a free zone was 100 percent foreign ownership. That advantage has largely equalised. Since the 2021 amendment to the Commercial Companies Law, full foreign ownership is the standard for the large majority of mainland commercial and industrial activities, with no Emirati majority partner required. A limited set of strategic-impact and security-sensitive sectors still carry ownership or licensing conditions, but for typical trading and service businesses, ownership is no longer a reason to favour one route over the other.

Corporate tax treatment by route

Tax is now the heart of the decision. The UAE applies a 9 percent federal corporate tax on taxable profits above AED 375,000 (about US$102,000), with the first AED 375,000 taxed at 0 percent. How that headline rate applies — and whether a 0 percent rate is available at all, depends heavily on the structure.

| Route | Corporate Tax Position | Key conditions |

|---|---|---|

| Mainland | Standard regime; no qualifying-income carve-out. | Standard regime; no qualifying-income carve-out. |

| Free zone (QFZP) | 0% on qualifying income; 9% on non-qualifying income | Must satisfy all Qualifying Free Zone Person conditions; the 0% rate is activity-based, with no AED 375,000 threshold applied to qualifying income. |

| Free zone (non-qualifying) | 9% above AED 375,000 | A free-zone company that fails QFZP conditions, or elects out, is taxed like a mainland company. |

| Large multinational groups (any route) | 15% minimum effective rate | Domestic Minimum Top-Up Tax applies to in-scope groups regardless of free-zone status. |

The mainland position

A mainland company is straightforward: profits above AED 375,000 (US$102,110) are taxed at 9 percent, with no qualifying-income concept. Smaller businesses may benefit from Small Business Relief, which can treat a company with revenue up to AED 3 million (US$816,900) as having no taxable income for the period, subject to election and conditions.

The free-zone position and the QFZP test

A free-zone company can access a 0 percent rate, but only on “qualifying income,” and only if it meets the conditions to be a Qualifying Free Zone Person (QFZP). In 2026 this is best understood not as a status conferred at registration, but as an annually tested position that must be actively maintained. The core conditions include maintaining adequate economic substance in the zone, earning qualifying income as defined by the regime, complying with transfer-pricing rules and arm’s-length pricing on related-party transactions, not electing into the standard regime, and staying within the de minimis limits on non-qualifying revenue.

That de minimis threshold caps non-qualifying income at the lower of 5 percent of total revenue or AED 5 million. Crucially, the consequences of failure are severe: breaching the conditions causes the company to lose QFZP status entirely — not just on the offending income stream — and to be taxed at 9 percent on all income for that tax period and, potentially, the four subsequent years. Most direct sales into the mainland market are treated as non-qualifying income. The 0 percent rate is therefore a conditional benefit to be protected through documentation and structuring, not an automatic feature of a free-zone licence.

Financial free zones — the DIFC and Abu Dhabi Global Market (ADGM) — receive the same federal corporate-tax treatment as other free zones, making them common homes for finance, fund, and family-office vehicles that can qualify for 0 percent on qualifying income under the same conditions.

The global minimum tax overlay

Large multinational groups face an additional layer that can override the free-zone advantage. Under the Domestic Minimum Top-Up Tax (DMTT), introduced via Cabinet Decision No. 142 of 2024 and clarified by updated Ministry of Finance guidance in late 2025, in-scope groups must pay a minimum effective tax rate of 15 percent on their UAE profits. The DMTT applies to multinational groups with consolidated global revenues of at least €750 million (roughly US$815 million) in at least two of the four preceding financial years, for financial years beginning on or after 1 January 2025. Purely domestic groups are excluded.

For these groups, a 0 percent free-zone rate may simply be “topped up” to 15 percent, so the headline UAE rates are only a starting point and group-level modelling is essential before committing to a structure.

Costs and timelines

Setup economics still differ by route, though the gap has narrowed. Free-zone packages typically bundle the licence with flexible-desk or office space and a set number of visa allocations, with entry-level costs starting near AED 12,500–15,000 (about US$3,400–4,100) in the lowest-cost zones and setup often completed in five to ten days. A low-cost mainland professional licence can come in around AED 10,000–14,000 (about US$2,700–3,800) before office and visa costs, with timelines more commonly in the two-to-four-week range and a physical office generally required.

Investors should compare the total cost of operation — including year-two renewals, office, and visa costs, and now the additional DET branch or permit fee where mainland access is needed — rather than the headline licence fee. Much of the registration for both routes can now be completed remotely through digital portals, though some banking and visa steps may still require an in-person visit.

Compliance

Whichever route an investor chooses, 2026 raises the compliance bar. The corporate tax filing and payment deadline for businesses with a December 31, 2025 financial year-end is September 30, 2026, and the free-zone qualifying-income guidance has matured to the point where a “qualifying” claim that no longer holds up under refined rules carries real audit exposure.

Free-zone companies must register with the Federal Tax Authority, file annual returns, and actively evidence their QFZP position; mainland companies must manage standard returns and documentation. A unified administrative penalty regime introduced in 2025 has further raised the cost of getting compliance wrong. For well-advised, transparent businesses, this tightening can function as a moat; for the unprepared, it is a growing risk.

Which route fits which investor?

There is no universal answer, but some patterns hold in 2026:

- A free zone tends to suit businesses whose income is predominantly international or business-to-business with other free-zone entities — international trade, holding structures, technology, professional services, and finance or fund vehicles in the DIFC or ADGM — where the 0 percent qualifying-income rate is achievable and worth the substance and compliance investment. The new mainland-access permit makes this route more flexible than before for firms that occasionally need to serve domestic clients.

- The mainland tends to suit businesses built around the UAE domestic market (retail, contracting, consumer services, hospitality, and government-facing work) where unrestricted local trade and the ability to bid for public contracts matter more than a conditional 0 percent rate, and where the simplicity of the standard 9 percent regime is an advantage.

- A combined structure (a free-zone entity with a DET mainland branch or permit, or parallel entities under common ownership) is increasingly viable for businesses that genuinely straddle both markets, though it requires careful coordination across tax, licensing, and substance to avoid duplicated cost or transfer-pricing risk.

For large multinational groups, the choice is shaped less by the 9 percent versus 0 percent question and more by the 15 percent global minimum tax, which can neutralise free-zone benefits and rewards group-level planning over entity-level rate shopping.

Conclusion

In 2026, “free zone versus mainland” is no longer a binary contest between tax-free convenience and full market access. Ownership has equalised, mainland access has opened up, and the real differentiators are now the availability and maintenance of the free-zone 0 percent rate, the activity profile of the business, the cost and burden of compliance, and (for the largest groups) the global minimum tax.

The investors who do best are those who treat the structuring decision as a tax and compliance question to be modelled at the outset, not a box ticked at registration.

How Dezan Shira & Associates can help

Dezan Shira & Associates supports foreign companies across the full investment lifecycle in the UAE, from choosing between mainland, free-zone, and financial-centre structures to entity setup, licensing, tax registration, and ongoing compliance.

Through our Dubai office, we help investors model the corporate-tax, QFZP, and substance implications of each route, register with the Federal Tax Authority for corporate tax and VAT, and keep entities compliant with UAE and Pillar Two obligations. To arrange a consultation, please contact our local advisory team.

About Us

Middle East Briefing is one of five regional publications under the Asia Briefing brand. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Dubai (UAE). Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in China (including the Hong Kong SAR), Indonesia, Singapore, Malaysia, Mongolia, Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to Middle East Briefing’s content products, please click here. For support with establishing a business in the Middle East or for assistance in analyzing and entering markets elsewhere in Asia, please contact us at dubai@dezshira.com or visit us at www.dezshira.com.

- Previous Article Setting Up a Business in Dubai: A 2026 Guide

- Next Article UAE End-of-Service Gratuity: How to Calculate It