Saudi Arabia’s Insurance Boom: Market Shifts, Growth Dynamics and Opportunities

Saudi Arabia’s insurance sector is expanding rapidly, driven by mandatory health and motor coverage, Vision 2030 projects, digitalization, and rising demand for risk protection.

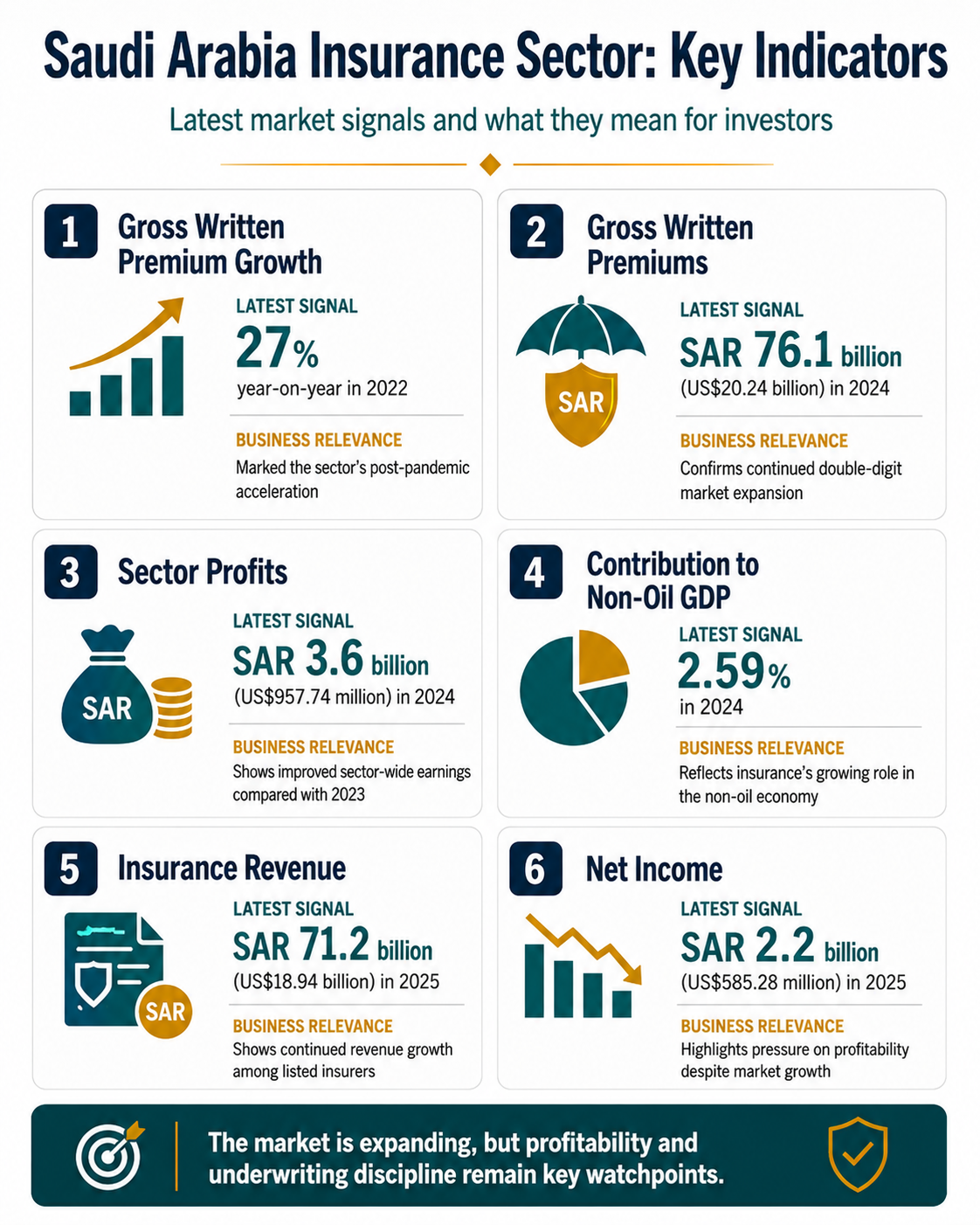

Saudi Arabia’s insurance sector is moving through one of its strongest growth phases in recent years. Gross written premiums increased by 27 percent year-on-year in 2022, marking a turning point for the market after the pandemic period. Growth has continued since then, with premiums reaching SAR 76.1 billion (US$20.24 billion) in 2024 and the sector’s contribution to non-oil GDP rising to 2.59 percent.

The expansion reflects more than higher demand for compulsory health and motor insurance. Insurance is becoming part of Saudi Arabia’s broader financial and economic infrastructure, supporting healthcare, mobility, infrastructure, real estate, logistics, tourism, and household financial planning. For insurers, reinsurers, brokers, insurtech firms, and foreign investors, the opportunity is significant.

However, the market is also becoming more competitive and more regulated. Premium growth has been strong, but profitability remains sensitive to claims inflation, pricing pressure, medical costs, reinsurance capacity, and underwriting discipline.

What is driving Saudi Arabia’s insurance growth?

Saudi Arabia’s insurance boom is being supported by several structural factors:

- Mandatory coverage: Health and motor insurance remain the largest and most established segments, supported by compulsory requirements and stronger enforcement.

- Economic diversification: Vision 2030 projects are creating demand for commercial insurance across construction, hospitality, logistics, real estate, entertainment, energy, and infrastructure.

- Higher risk awareness: Businesses and households are increasingly using insurance as a financial protection tool rather than only a regulatory obligation.

- Regulatory development: The Insurance Authority is strengthening sector oversight, product regulation, market conduct, and policyholder protection.

- Digitalization: Online distribution, claims automation, digital brokers, and data-driven underwriting are changing how products are sold and managed.

- Reinsurance needs: Larger infrastructure and commercial risks are increasing demand for stronger reinsurance capacity and technical underwriting.

Together, these drivers point to a market that is expanding in size and becoming more sophisticated in structure.

Key segments in Saudi Arabia’s insurance sector

Health insurance remains the market anchor

Health insurance remains the market anchor

Health insurance is the largest and most important segment in Saudi Arabia’s insurance market. It is supported by mandatory employer coverage, the expansion of private healthcare, population growth, and rising use of medical services.

However, health insurance is also one of the most operationally demanding segments. Insurers must manage provider networks, medical inflation, claims approval, fraud risk, and customer expectations. Premium growth alone will not be enough to protect margins. Companies with stronger claims management, data analytics, provider coordination, and pricing discipline will be better positioned.

For foreign investors and service providers, the health segment offers opportunities in:

- Third-party administration: Supporting insurers and employers with claims and benefit management;

- Digital health integration: Linking insurance products with healthcare platforms and provider networks;

- Medical cost analytics: Helping insurers assess utilization, pricing, and claims trends;

- Fraud detection: Using data tools to identify irregular claims and reduce leakage; and

- Employee benefits advisory: Supporting companies with medical coverage design and compliance.

Motor insurance: Scale with margin pressure

Motor insurance remains one of Saudi Arabia’s most visible insurance lines, supported by compulsory coverage and stronger digital enforcement. Online comparison platforms, digital distribution, and vehicle ownership trends have increased market accessibility.

The challenge is profitability. Motor insurance can be exposed to aggressive pricing, repair cost inflation, fraud, and claims leakage. The next phase of growth will depend less on policy volume and more on underwriting quality, claims efficiency, and better risk selection.

Key opportunities include:

- Digital claims processing: Reducing settlement times and improving customer experience;

- Repair network integration: Controlling costs through approved service providers;

- Telematics: Pricing policies based on driver behavior and usage;

- AI-enabled fraud detection: Identifying suspicious claims patterns earlier; and

- Fleet risk management: Supporting logistics, mobility, and corporate vehicle operators.

Property, casualty, and project-linked insurance

Saudi Arabia’s infrastructure and real estate pipeline is creating demand for more sophisticated property and casualty insurance. Large-scale projects in tourism, logistics, energy, entertainment, transport, hospitality, and industrial development require stronger risk coverage.

This is creating demand for products such as:

- Construction all-risk insurance;

- Engineering insurance;

- Professional indemnity;

- Marine cargo insurance;

- Liability coverage;

- Property insurance;

- Business interruption insurance; and

- Specialist project risk products.

This segment is particularly relevant for foreign insurers, reinsurers, brokers, and risk consultants. Technical expertise, local partnerships, and regulatory familiarity will be important, especially for complex project risks and large corporate accounts.

Protection and savings: A long-term growth area

Protection and savings insurance remains smaller than health and motor, but it is becoming more relevant. As household wealth grows and financial planning becomes more sophisticated, demand may increase for long-term savings, life protection, retirement-linked products, and employee benefit solutions.

This segment is still developing, which means growth will depend on awareness, distribution, product design, and trust. Insurers that can provide simple, transparent, and digitally accessible products may be able to capture early market share.

Potential opportunities include:

- Long-term savings products;

- Life and protection insurance;

- Retirement-linked solutions;

- Employee benefit packages;

- Family protection plans; and

- Digitally distributed savings products.

Reinsurance and local capacity

As Saudi Arabia’s insurance market grows, reinsurance is becoming more strategic. Larger projects, more complex commercial risks, and higher policy limits require deeper risk capacity and stronger technical modelling.

The development of domestic retention and reinsurance capability is also important for the Kingdom’s broader financial sector ambitions. Retaining more risk locally can help build expertise, deepen capital markets, and reduce reliance on external capacity for certain lines.

Priority areas include:

- Catastrophe modelling;

- Cyber risk;

- Engineering and infrastructure risks;

- Large commercial accounts;

- Actuarial reserving;

- Risk-based pricing; and

- Portfolio analytics.

This creates opportunities for reinsurers, actuarial firms, risk modelling specialists, and advisory providers that can support technical underwriting and capital management.

Opportunities for foreign investors

Saudi Arabia’s insurance sector offers several market-entry and expansion opportunities

| Investor type | Potential opportunity |

| Insurers | Product expansion, specialist lines, partnerships, corporate accounts |

| Reinsurers | Large risks, infrastructure projects, retention capacity, specialist underwriting |

| Brokers | Corporate risk, SME coverage, project insurance, employee benefits |

| Insurtech firms | Digital distribution, claims automation, analytics, embedded insurance |

| Actuarial and advisory firms | Reserving, pricing, capital modelling, regulatory support |

| Healthcare service providers | Claims management, provider networks, medical cost control |

| Risk consultants | Construction, energy, logistics, cyber, business interruption |

The most attractive opportunities are likely to be in areas where demand is rising and technical capability is still developing. These include healthcare administration, corporate risk, reinsurance, claims technology, digital distribution, and specialist insurance lines.

How Dezan Shira & Associates can help

About Us

Middle East Briefing is one of five regional publications under the Asia Briefing brand. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Dubai (UAE). Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in China (including the Hong Kong SAR), Indonesia, Singapore, Malaysia, Mongolia, Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to Middle East Briefing’s content products, please click here. For support with establishing a business in the Middle East or for assistance in analyzing and entering markets elsewhere in Asia, please contact us at dubai@dezshira.com or visit us at www.dezshira.com.

- Previous Article UAE Golden Visa in 2026: The Four Routes, the New Rules, and Which One Fits You

- Next Article